What are Islamic Mortgages and how do they work?

A guide to how Islamic mortgages work. Murabaha, Ijara, and Diminishing Musharaka explained, plus how they compare to conventional mortgages.

Islamic mortgages are starting to become a meaningful part of the home finance market in the UK, and the West in general. Despite this, they're often seen as the same as conventional mortgages but just religiously branded, higher-cost alternatives. There is real demand for these products, but these doubts are why uptake remains slow.

The end result may look the same on paper, but the mechanics behind the products are very different. Islamic mortgages aim to achieve two main goals that distinguish them from their conventional counterparts:

To not generate income via Riba (Interest)

Asset-backed risk sharing

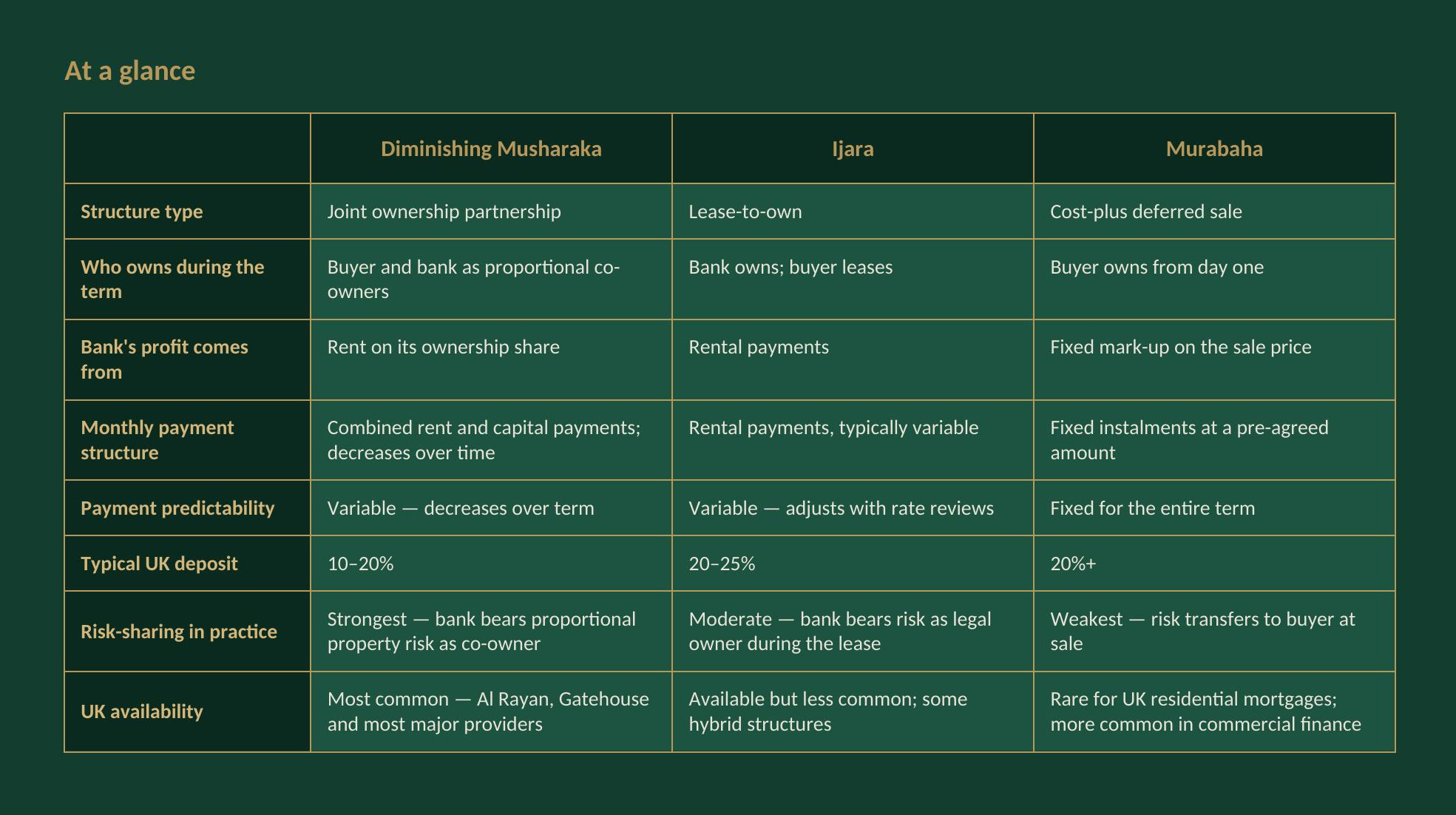

Both of these goals aim to achieve a fairer and more sustainable alternative form of property ownership, one that balances risk with reward for each party. In practice this is achieved via three main structures: A Diminishing Musharaka, an Ijara or a Murabaha.

Below I will examine how these three structures work, practical considerations buyers may face and an honest assessment of where Islamic mortgages genuinely deliver on their principles versus where the gap between theory and practice shows.

Lets start with the most common form of Islamic mortgage, Diminishing Musharaka.

Diminishing Musharaka - Partnership

A Musharaka refers to a joint venture, or a partnership. In the context of an Islamic Mortgage, the individual seeking to buy a property engages in a partnership with an Islamic Bank/Lender.

These two parties have different risk profiles, capital levels and objectives when it comes to owning a property. One wants to own a property but does not have enough spare capital to outright buy it. The other has significant capital stores, and aims to conduct profit-generating, financing ventures. They however, have no need for this property.

These two parties therefore form a partnership to pool capital and then buy this asset together. The latter however does not want to retain its possession of the property and so over time, the former buys out its share of this partnership, (hence the diminishing aspect).

This is the most common form of Islamic Mortgage we see today in the market, often referred to as a home purchase plan (HPP). A theoretic illustrative example is detailed below;

The buyer and bank become joint owners of the property. The buyer contributes a deposit of typically 10-20% of the property value, and the bank funds the remaining 80-90%. Both parties hold proportional ownership stakes in this example. The deposit serves a similar purpose to a conventional mortgage deposit: providing a safety buffer and signalling buyer commitment.

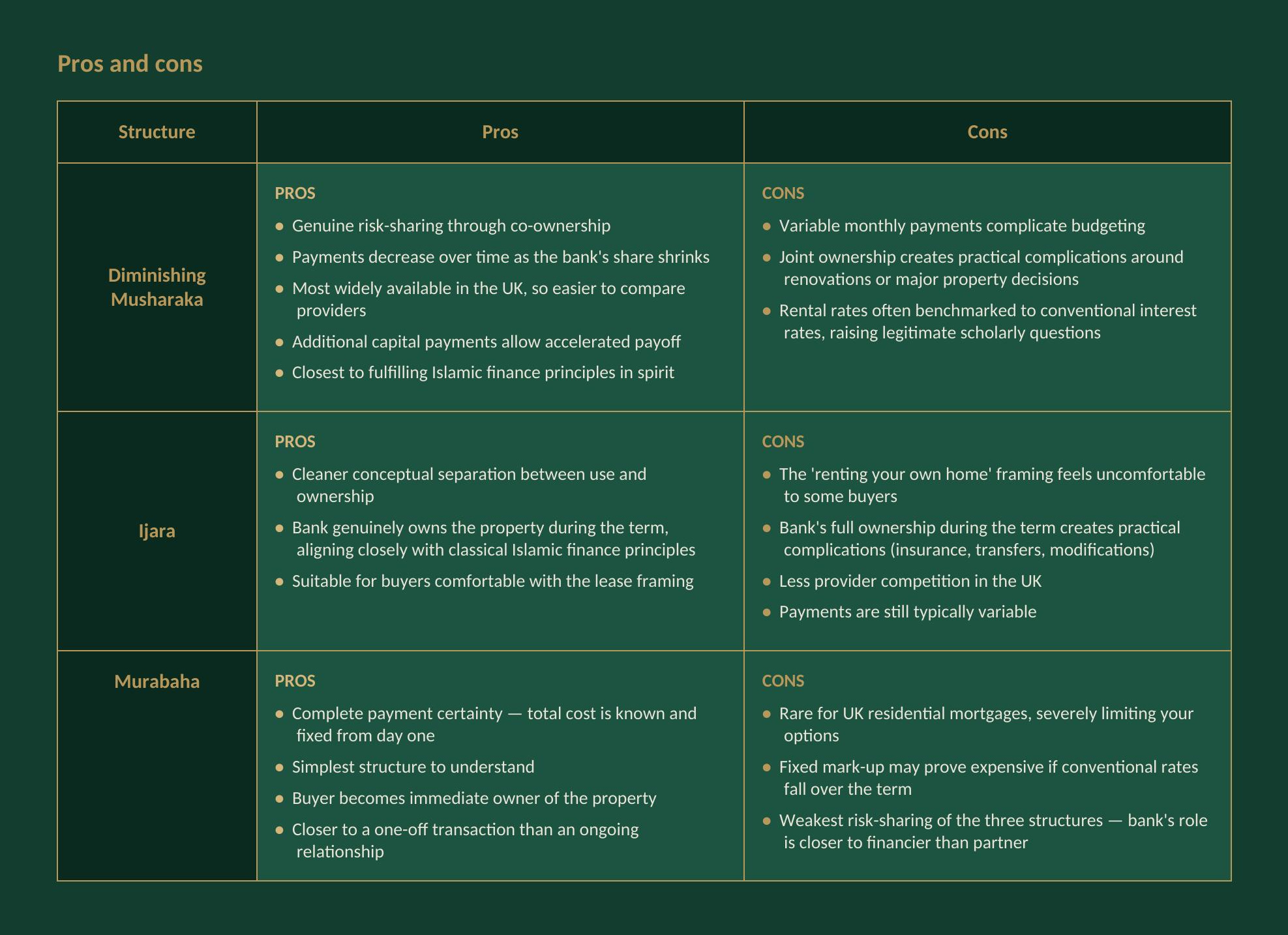

The buyer occupies and uses the property; the bank earns rent on its share. Because only the buyer benefits from living in the property, the bank is entitled to compensation for its ownership share. This compensation takes the form of rent, charged proportionally to the bank’s stake. As the bank’s share decreases over the term, the rent it charges decreases in parallel (assuming a stable rental rate). The practical reality is more complex, as I'll cover later.

The buyer makes capital payments to acquire the bank’s share gradually. Alongside the rent, the buyer makes scheduled capital payments that progressively buy out the bank’s stake. In practice, the rent and capital payments are combined into a single monthly payment, which (in theory) typically decreases over time as the rental component shrinks. Buyers can usually make additional capital payments to acquire the bank’s share faster.

At the end of the term, the buyer owns 100% of the property. The bank’s share has been fully acquired, ownership is consolidated in the buyer’s name, and no further rent is payable. The structure has run its course.

The risk-sharing principle plays out across the term: because the bank is a genuine co-owner during the term, it bears proportional risk if the property value falls. For instance, in the event of a forced sale at a loss, both parties absorb proportional losses. This is structurally different from conventional mortgages, where the borrower bears all of the property risk regardless of who funded the purchase.

Ijara - lease

An Ijara is essentially a lease-to-own scheme. The lender here buys the property and leases it out to you for use. As with standard property leases, you pay rent during the lease period. You however can also agree to also buy back the property and shift ownership, as the bank owns the property until the end of the term. This could be done as a balloon payment at the end of the period, but more practically you would pay capital repayments alongside your rental payments within your monthly payments, similar to the payment schedule seen in Diminishing Musharaka.

The rental rate that is charged for this lease is variable, and period adjustments and repricing are allowed during the lifetime of the transaction.

The conceptual difference from Diminishing Musharaka is that the bank fully owns the property during the term rather than being a co-owner with you. Some find this cleaner from a Shariah perspective there's no joint ownership to navigate, and the relationship is more straightforwardly a lease. Others find the 'renting your own home' framing uncomfortable. In practice, Ijara products often involve hybrid structures with elements borrowed from Diminishing Musharaka, blurring the conceptual distinctions.

Murabaha - Cost Plus

A less popular form of financing is the cost plus sale, Murabaha. Here the Islamic bank buys the property from a landlord for the agreed price, then immediately sells it onwards to you at a higher price (the original price plus a fixed mark-up representing the bank’s profit). You would typically pay this back in instalments over the agreed term. The profit the bank plans to make is clearly disclosed in the contract (a requirement according to Shariah principles).

Suppose you want to buy a £300,000 house with a £30,000 deposit. The bank purchases the property for £270,000 (the amount being financed) and agrees to sell it to you for a fixed total of, say, £405,000, a markup of £135,000, representing the bank's profit. This total is fixed and disclosed in the contract from day one. You pay this £405,000 back in fixed monthly instalments over 15 years, working out to roughly £2,250 per month.

Whether conventional interest rates rise or fall over those 15 years, your payment doesn't change, and your total obligation is known on day one. The 'markup' translates to roughly the equivalent annualised rate of around 6% here, but it's structurally different. It's a fixed price for a fixed asset, not a compounding interest charge.

This is akin to a fixed-rate conventional mortgage. The key Shariah distinction is that the price was set at the moment of sale rather than accumulated as interest over time, increasing transparency in the transaction.

Murabaha is rare for residential mortgages because the fixed total cost makes the bank carry the interest rate/markup risk over a long term, if conventional rates rise, the bank effectively under-prices its product; if they fall, the buyer feels overcharged. Murabaha is more common for shorter-term financing or commercial transactions.

Comparing the three structures

The key defining elements of these structures can be summarised below:

As highlighted above, the most commonly used method in current markets as an Islamic Mortgage alternative is the Diminishing Musharaka model. It is the model that structurally makes the most sense for this type of financing agreement. It is the most digestible to western consumers as in form (not substance), it mirrors conventional mortgages. There are however pros and cons to each of these structures that should perhaps be considered so I have highlighted these below:

A comparison between each other has been made above, but how do these compare against a conventional mortgage? Moving forward , I will treat Islamic Mortgages as synonymous with Diminishing Musharaka given it is the most common form. There are two main areas where the comparison gets interesting: the role of the lender, and what happens when things go wrong.

Islamic Mortgage vs Conventional Mortgage

The main comparisons, as highlighted in this article and other articles on my page, is the fact that in an Islamic Mortgage, the lender shares ownership in the property and does not charge interest as it is not a loan. The former comparative is important as it enforces a vested interest in the property from the lender which in turn encourages them to operate in the best interest of both parties.

In a conventional mortgage, the bank is less concerned for the outcome of the property and whether it devalues/ gets damaged as they don’t share in the upside or downside like a co-owner would. The would care indirectly as it could signal late payments or defaults and would potentially have to recover a devalued asset. But the ‘skin in the game’ is not nearly as prevalent.

The latter comparative however seems as though interest has been repackaged as rent. In theory this is not a valid argument as rent is pegged to the value of the banks share of the property and so the non-capital repayments will decrease over time unlike mortgages (which are usually fixed for the term of the loan).

The reality however is that most Islamic Mortgage providers currently benchmark the rental rate to interest rates (historically LIBOR, now SONIA or other reference rates). These are periodically reviewed to ensure they are in line with these benchmarks. This is a genuine shortfall with the product we see in today’s market as there is a mismatch with the theory.

There is however still a meaningful structural difference in the instances of missed payments.

In a conventional mortgage the missed payment becomes "arrears" , an outstanding amount you now owe on top of your regular payments. Interest continues to accrue on the full outstanding mortgage balance, including arrears, at your normal mortgage rate. Your lender will typically charge administrative fees for late payments and arrears handling fees. After a few missed payments, the lender may start formal collection actions, eventually leading to repossession proceedings.

In an Islamic Mortgage however the rent component represents payment for the bank’s continued ownership of part of the property. When you miss a rent payment, you owe the bank that rent but, crucially, the rent doesn’t compound or accrue additional charges in the same way. Islamic finance principles prohibit charging additional fees for late payment because that would constitute riba (charging more money for the passage of time on a debt).

Instead the missed rent becomes a debt to the bank. Under Shariah principles, the bank cannot legitimately charge interest on this missed payment. The bank can charge actual administrative costs incurred (real costs of chasing the payment), but these are typically modest and capped.

Some Islamic mortgage providers may charge a “late payment donation” which goes to charity rather than to the bank as profit, a Shariah-compliant workaround that some providers use, though scholars disagree on whether this is genuinely different in substance.

If the buyer continues to miss payments and the situation becomes serious, the bank still has remedies, the property is jointly owned, and the bank can ultimately force a sale to recover its share. But during the missed-payment period itself, the buyer’s obligation doesn’t balloon in the way it might with compounding interest.

How expensive are Islamic Mortgages though?

There are several practical considerations that need to be considered for an Islamic Mortgage. The most glaring and obvious of these being the cost.

There's a noticeable premium: providers have historically charged rates 0.5–1.5 percentage points above comparable conventional mortgages. This is a real additional cost that could translate from hundreds, to thousands in annual price differentials.

This premium exists mainly because of the smaller market scale (fewer providers, less competition), and also a lack of economies of scale the larger banks have access to. They also have more complex underlying structures (more legal and administrative work per mortgage) and in some cases Shariah governance costs.

Whether the premium is “worth it” , I believe, ultimately depends on whether you accept the Islamic finance principles. For Muslim buyers who consider conventional mortgages religiously impermissible, the premium is the cost of compliance with their values. For non-Muslim buyers attracted to ethical finance principles, there is maybe not as strong of a pull here.

The industry is however still young and in its growth stage. The premium will likely narrow as the market matures, and competitive dynamics between providers have improved. At the time of writing this there are only a handful of providers but this has grown from almost no providers in the past 10 years alone. The market needs time and it needs investment, and with this I genuinely believe a better product will exist, which will attract both Muslims and non Muslims alike.

For specifics on rates and provider comparisons, please stay tuned for future articles.

Other Practical Considerations

Above and beyond the cost, there are a number of other considerations to be made with current product offerings. I have briefly covered these below:

Deposit requirements : Typically higher than conventional minimums. Expect to need 10-20% rather than the 5-10% minimums available on conventional mortgages, though this varies by provider and product.

Eligibility criteria: Standard credit, income, and affordability checks similar to conventional mortgages. Some providers have specific requirements around income source (some won’t accept income from impermissible industries) but this is increasingly rare. However, some providers (e.g. StrideUp) currently also have more flexible criteria when it comes to contractors and self employed applicants, compared to conventional mortgages.

The application process: Broadly similar to conventional mortgages with similar timelines (typically 6-12 weeks from application to completion). Documentation requirements are similar.

Property restrictions: Some providers restrict the types of properties they’ll finance (no leasehold properties below certain remaining lease lengths, no shared ownership in some cases, restrictions on properties used for impermissible purposes).

Remortgaging and moving home: Generally possible but sometimes more complex than with conventional mortgages, particularly if you’re moving to a property the same provider doesn’t finance. Worth considering before committing.

What happens if you get into financial difficulty : Same FCA consumer protections apply. The mechanism for repossession is structurally different (since the bank already owns part or all of the property in many structures) but the practical experience for the buyer is broadly similar.

Insurance: You typically need buildings insurance just as with conventional mortgages, though the specific arrangements may differ slightly because of the joint ownership structure.

So should you get an Islamic Mortgage?

Short answer: It depends.

Long answer: Islamic Mortgages genuinely deliver on a number of fronts. Firstly structural risk-sharing is real. Banks bear property risk in ways conventional lenders don’t, which is inherently a more equitable product setup.

Shariah governance is also genuine (qualified boards / scholars review and sign off on these products), and for buyers who consider conventional mortgages religiously impermissible, these products provide an actual legitimate alternative to consider.

The current product setup however is far from perfect. Rental rates often track conventional interest rate movements closely, raising questions about how structurally different the products really are economically. Some scholars criticise specific aspects of the mortgages as they are too closely mimicking conventional products.

There’s ongoing disagreement among Islamic finance scholars about whether contemporary Islamic mortgages fully meet the spirit of Islamic finance principles or just the letter. This isn’t necessarily a reason to avoid them, but it’s a reason to engage thoughtfully rather than assume they’re either perfect or fraudulent.

My Opinion

If you are Muslim, desire to adhere to your religious beliefs and can afford it, I would encourage you to get an Islamic Mortgage. They are meaningfully different in structure and allow for a more balanced and equitable approach to home financing. It is not perfect in the eyes of the Shariah, but it is the closest thing to it.

At this stage of its life cycle this product needs the demand so that the providers can start to benefit from economies of scale and become more competitive against conventional banks. The Muslim population is seriously underserved for Shariah compliant alternatives. The higher participation in this market, the better these products can serve.

Competition in the industry drives prices down as participants vie for market share. It can also help flourish the product itself and allow for technical innovations to be made, that create even further justifications for this being a worthy alternative for every mortgage consumer.

As the industry evolves, I believe compromises will also be less common with there a) being less of an economic need to do so but also b) Shariah compliance requirements will likely become more stringent. This will steer the product to be more aligned with its purer form.

If you are not Muslim, the argument is harder to make here. I do believe regardless of faith, these products in essence, can be much better alternatives to conventional products. As of right now, they aren’t quite there yet.

If you are however still interested in the potential of this product, I urge you to keep an eye on the market and consider it a possibility. Especially later down the line as the market matures and converges to a more robust and structurally sound outcome.

In future posts I will look more closely at what current offerings there actually are in the market, covering current rates, fee structures, customer experiences and eligibility from the key players

Please stay tuned and subscribe to get that article when published.

Thanks for reading,

Aqila Finance.